Top 5 Insurance Types Every Small Business Should Consider

Running a small business involves numerous risks, making it essential to protect your investment with the right insurance. Here are the top 5 insurance types every small business should consider:

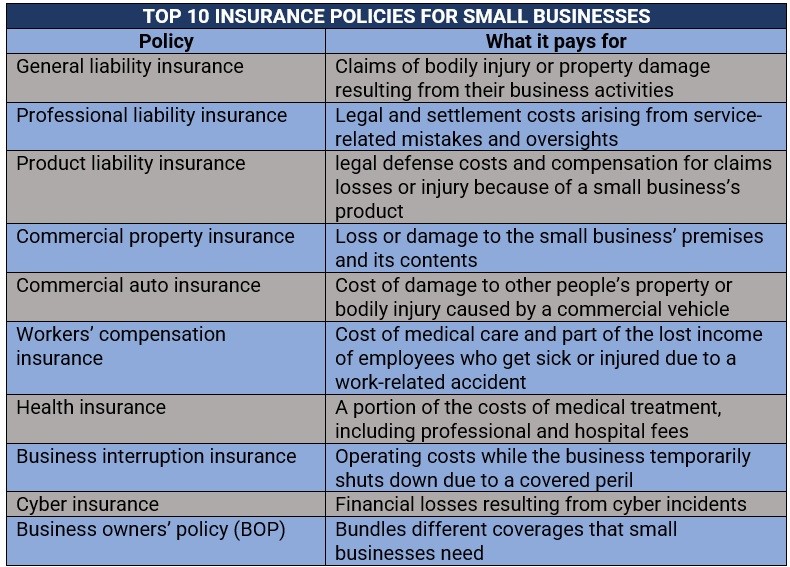

- General Liability Insurance: This is the cornerstone of business insurance, covering claims related to bodily injury, property damage, and personal injury. It protects your business from lawsuits that can arise from accidents on your property or due to your business operations.

- Property Insurance: If your business owns physical assets, this insurance safeguards against damages like fire, theft, or natural disasters. Whether you operate from a rented space or own your building, property insurance is vital.

- Business Interruption Insurance: This type of insurance helps cover lost income during periods of disruption due to unforeseen events, such as natural disasters. It ensures that your small business can continue to pay bills and staff even when operations are temporarily halted.

- Workers' Compensation Insurance: Required in most states, this insurance covers medical expenses and lost wages for employees who get injured on the job. It not only protects your employees but also shields your business from legal complications.

- Professional Liability Insurance: Also known as errors and omissions insurance, this type protects your business against claims of negligence or inadequate work. If you're in a service-based industry, this coverage is crucial for maintaining your professional reputation.

How to Choose the Right Insurance Coverage for Your Small Business

Choosing the right insurance coverage for your small business is crucial to ensuring its long-term success and stability. Start by assessing the specific needs of your business based on factors such as industry type, company size, and potential risks. Consider the following types of coverage that are commonly recommended for small businesses:

- General Liability Insurance: Protects against claims of bodily injury or property damage.

- Property Insurance: Covers damage to your business property, including equipment and inventory.

- Worker's Compensation Insurance: Essential for businesses with employees, this covers medical costs and lost wages for work-related injuries.

Once you have identified the types of coverage necessary, it's important to compare different policies and providers. Look for a reputable insurance company that specializes in small business insurance and offers customizable options to fit your specific needs. Cost is an important factor, but it shouldn't be the only consideration—evaluate coverage limits, exclusions, and customer service ratings. Don't hesitate to consult with an insurance advisor for expert guidance to ensure you make the best choices for your business.

Is Your Small Business Protected? Common Insurance Mistakes to Avoid

As a small business owner, ensuring that your enterprise is adequately protected is essential for long-term success. However, many entrepreneurs fall into common insurance traps that can leave them vulnerable. One prevalent mistake is underinsuring your business property. While it may seem financially prudent to save on premiums by selecting minimal coverage, this approach can result in significant losses in the event of a disaster. Regularly reassessing the value of your assets and adjusting your policy accordingly is crucial. Additionally, many small businesses overlook the importance of general liability insurance, which can protect against claims related to bodily injury or property damage.

Another common error is failing to understand the nuances of workers' compensation insurance. Some business owners mistakenly believe that this coverage is only necessary for larger companies, when in fact, it is crucial for small businesses as well. Not having adequate workers' compensation can lead to severe financial repercussions if an employee gets injured on the job. Moreover, reviewing your insurance policy regularly and discussing options with a knowledgeable agent can prevent unexpected gaps in coverage. By taking these important steps, small businesses can protect themselves from the unforeseen challenges that may arise.